CHAPTER 1

AN INTRODUCTION WORTH READING

Champions aren’t made in the gyms. Champions are made from something deep inside them—a desire, a dream, a vision.

- AN INTRODUCTION WORTH READING

- Follow Your Dreams and Believe in Yourself

- And the Trade Shall Set You Free

- Achieving the Best of Both Worlds

- CHAPTER 4

- VALUE COMES AT A PRICE

- The P/E Ratio: Overused and Misunderstood

- Bottom Fishers’ Bliss

- The Cheap Trap

- Don’t Pass on High P/E Stocks

- High Growth Baffles the Analysts

- CHAPTER 7

- FUNDAMENTALS TO FOCUS ON

- FOLLOW THE LEADERS

- RISK MANAGEMENT

- PART 2: HOW TO DEAL WITH AND CONTROL RISK

— Muhammad Ali, three-time world heavyweight boxing champion

IN THE HEAT OF COMPETITION, champions rise to their strengths, triumphing over mere contenders. Marathon runners win through superior endurance and a keen sense of pacing. The great flying aces of World War I defeated their enemies, winning dogfights by thinking faster and better in three-dimensional space. At the chessboard, victory goes to the player who sees more clearly through the maze of possible moves to unlock the winning combination. Virtually every human contest is dominated by the few who possess the unique traits and skills required in their fields. The stock market is no different. Trade Like a Stock Market Wizard

Investing styles may differ among successful market players, but without exception, winning stock traders share certain key traits required for success. Fall short in those qualities and you will surely part ways with your money. The good news is that you don’t have to be born with them. Along with learning effective trading tactics, you can develop the mindset and emotional discipline needed to win big in the stock market. Two things are required: a desire to succeed and a winning strategy. In *Trade Like a Stock Market Wizard: How to Achieve Superperformance in Stocks in Any Market*, I

will show you how my winning strategy brought me success and how it can do the same thing for you.

I’ve been trading and investing in the stock market for most of my adult life: 30 years and counting as of the writing of this book. Stock trading is how I made my living and ultimately my fortune. Starting with only a few thousand dollars, I was able to parlay my winnings to become a multimillionaire by age 34. Even if I had not become rich from trading stocks, I would still be doing it today. For me, trading isn’t a sport or just a way to make money; trading is my life.

I didn’t start out successful. In the beginning, I made the same mistakes every new investor makes. However, through years of study and practice, I gradually acquired the necessary know-how to achieve the type of performance you generally only read about. I’m talking about *superperformance*. There’s a big difference between making a decent return in the stock market and achieving superperformance, and that difference can be life-changing. Whether you’re an accountant, a schoolteacher, a doctor, a lawyer, a plumber, or even broke and unemployed as I was when I started, believe me you can attain superperformance.

Success requires opportunity. The stock market provides incredible opportunity on a daily basis. New companies are constantly emerging as market leaders in every field from high-tech medical equipment to retail stores and restaurants right in your own neighborhood. To spot them and take advantage of their success you must have the know-how and the discipline to apply the proper investment techniques. In the following pages, I’m going to tell you how to develop the expertise to find your next superperformer.

Follow Your Dreams and Believe in Yourself

Impossible is just a big word thrown around by small men who find it easier to live in the world they’ve been given than to explore the power they have to change it.

— Laila Ali

Dedication and a desire to succeed are definitely requirements to achieve superperformance in stocks. What is not required is conventional wisdom

or a college education. My real-world education began when I was an adolescent. I dropped out of school in the eighth grade at age 15, which means that I am almost completely self-educated. Yes, you read that correctly. I left school at age 15. I have never seen the inside of a high school as a student, let alone attended a university. What I did have, however, was a thirst for knowledge and a burning desire to succeed, to be the best trader I could be. I became a fanatical student of the stock market, its history, and human behavior. I started out by reading the financial news and stock reports at the local library. Over the years, I’ve read an incredible number of investment books, including more than 1,000 titles in my personal library alone.

In light of my lack of starting resources and formal education, the level of success I have achieved strikes some people as unlikely or even impossible. Along the way, some have even tried to discourage me. You too probably will face people who will try to dissuade you from trying. You will hear things such as “It’s a rigged game,” “You’re gambling,” and “Stocks are too risky.” Don’t let anyone convince you that you can’t do it. Those who think it’s not possible to achieve superperformance in stocks say so only because they never achieved it themselves, and so it’s hard for them to imagine. Ignore any discouragement you may encounter and pay attention instead to the empowering principles I am about to share with you. If you spend time studying and applying them, you too can realize results that will amaze even the most ambitious positive thinkers. Then the same people who said it couldn’t be done will ask you the question they always ask me, “How did you do it?”

And the Trade Shall Set You Free

From the very beginning, I saw the stock market as the ultimate opportunity for financial reward. Trading also appealed to me because I liked the idea of having the freedom to work at home and taking responsibility for my own success. In my young adult years, I had tried several different business ventures, and even though I felt enthusiastic, that passion was still missing. Finally, I came to realize that what I was most passionate about was freedom—freedom to do what I want, when I want, where I want.

One day it dawned on me: life is rich even if you’re not. I realized that things were happening every day, good and bad, and that it was just a matter

of deciding what I wanted to be part of. People were getting rich in the stock market. I said to myself, Why not be part of that? I figured that if I learned how to invest in the market and trade successfully, I could achieve my dream of financial freedom and, more important, personal freedom. Besides, who was going to hire a junior high school dropout? The stock market was the one place I could see that had unlimited potential without prejudice. The author and successful businessman Harvey Mackay said it perfectly, “Optimists are right. So are pessimists. It’s up to you to choose which you will be.”

Achieving the Best of Both Worlds

When I started trading in the early 1980s, I had only a few thousand dollars to invest. I had to make huge returns on my relatively small account to survive and still have some trading capital left. This forced me to hone my timing and learn the necessary tactics for extracting consistent profits out of the stock market day in and day out. Like a pro poker player who grinds out a steady living while consistently building a bankroll, I became a stock market “rounder.”

My philosophy and approach to trading is to be a conservative aggressive opportunist. Although this may seem like a contradiction in terms, it is not. It simply means that my style is to be aggressive in my pursuit of potential reward and at the same time be extremely risk-conscious. Although I may invest or trade aggressively, my primary thought process begins with “How much can I lose?” not just “How much can I gain?”

During my 30 years as a stock trader, I’ve discovered that a “risk-first” approach is what works best for me. It has allowed me not just to perform or perform well but to achieve superperformance, averaging 220 percent per year from 1994 to 2000 (a 33,500 percent compounded total return), including a U.S. Investing Championship title in 1997. My approach also proved invaluable when I needed it the most: cashing me out ahead of eight bear markets, including two of the worst declines in U.S. stock market history. By adhering to a disciplined strategy, I was able to accomplish the most important goal of all: to protect my trading account and keep the profits I made during the previous bull markets.

CHAPTER 4

VALUE COMES AT A PRICE

It’s far better to buy a wonderful company at a fair price than a fair company at a wonderful price.

— Warren Buffett

WHEN YOU THINK OF VALUE in the traditional sense, bargains immediately spring to mind: something once priced higher now is priced lower. It seems logical. Growth stock investing, however, can turn this definition on its head. In the stock market, what appears cheap could actually be expensive and what looks expensive or too high may turn out to be the next superperformance stock. The simple reality is that value comes at a price.

The P/E Ratio: Overused and Misunderstood

Every day, armies of analysts and Wall Street pros churn out thousands of opinions about stock values. This stock is overvalued; that one is a bargain. What is the basis of many of these valuation calls? Often it’s the price/earnings ratio (P/E), a stock’s price expressed as a multiple of the company’s earnings. A great amount of incorrect information has been written about the P/E ratio. Many investors rely too heavily on this popular formula because of a misunderstanding or a lack of knowledge. Although it may come as a surprise to you, historical analyses of superperformance stocks suggest that by themselves P/E ratios rank among of the most useless statistics on Wall Street.

The standard P/E ratio reflects historical results and does not take into account the most important element for stock price appreciation: the future. Sure, it’s possible to use earnings estimates to calculate a forward-looking P/E ratio, but if you do, you’re relying on estimates that are opinions and often turn out to be wrong. If a company reports disappointing earnings that fail to meet or beat the estimates, analysts will revise their earnings projections downward. As a result, the forward-looking denominator—the *E* in P/E—will shrink, and assuming the *P* remains constant, the ratio will rise. This is why it’s important to concentrate on companies that are reporting strong earnings, which then trigger upward revisions in earnings estimates. Strong earnings growth will make a stock a better value.

Bottom Fishers’ Bliss

Some analysts will recommend that you buy a stock that has had a severe decline. The justification may be that the P/E is at or near the low end of its historical range. In many instances, however, such price adjustments antici-

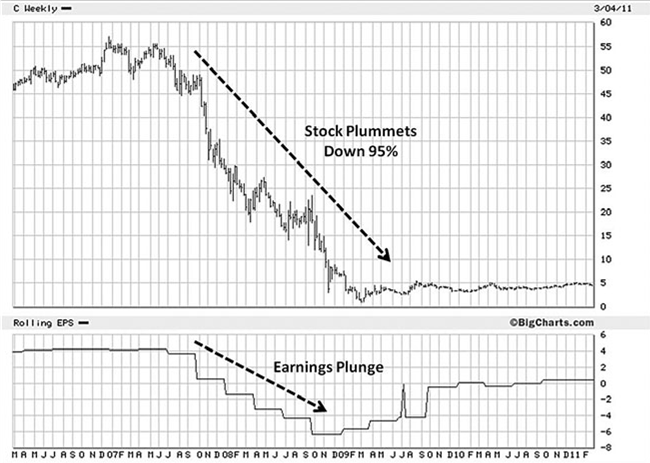

pate poor earnings reports. When quarterly results are finally released and a company misses analysts’ estimates or reports a loss, the P/E moves back up (in some cases it skyrockets), which may cause the stock price to adjust downward even further. This was the case for Morgan Stanley (MS/NYSE) in late 2007. The stock price fell and drove the P/E to a 10-year low. Morgan later reported disappointing negative year-over-year earnings comparisons, and the P/E ratio promptly soared to more than *120* times earnings. With earnings deteriorating and the stock selling at a P/E of 120, the stock was suddenly severely overvalued. The share price plunged even further to under $7. The cause of Morgan Stanley’s decline was an industrywide financial crisis, and by 2008 the P/E ratios of Bank America, Citigroup, and AIG all hit 10-year lows, along with those of many others in the banking and financial sector. Within 12 months, all three stocks plunged more than 90 percent.

The Cheap Trap

Buying a cheap stock is like a trap hand in poker; it’s hard to get away from. When you buy a stock solely because it’s cheap, it’s difficult to sell if it moves against you because then it’s even cheaper, which is the reason you bought it in the first place. The cheaper it gets, the more attractive it becomes based on the “it’s cheap” rationale. This is the type of thinking that gets investors in big trouble. Most investors look for bargains instead of looking for leaders, and more often than not they get what they pay for.

Don’t Pass on High P/E Stocks

It is normal for growth stocks to fetch a premium to the market; this is especially true if a company is increasing its earnings rapidly. Shares of fast-growing companies can trade at multiples of three or four times the overall market. In fact, high growth leaders can command even higher premiums in times when growth stocks are in favor relative to value stocks. Even during periods when growth is not in favor, they can sell at a significant premium to the market.

In many cases, stocks with superperformance potential will sell at what appears to be an unreasonably high P/E ratio. This scares away many ama-

teur investors. When the growth rate of a company is extremely high, traditional valuation measures based on the P/E are of little help in determining overvaluation. However, stocks with high P/E ratios should be studied and considered as potential purchases, particularly if you find that something new and exciting is going on with the company and there’s a catalyst that can lead to explosive earnings growth. It’s even better is if the company or its business is misunderstood or underfollowed by analysts.

Internet providers were a great example. When Yahoo! was at the forefront of one of the greatest technological changes since the telephone, I was asked in a television interview if I thought the Internet would survive. Can you imagine the Internet failing to exist? Not today. But in the early to middle 1990s you might have had a different view, as many did. That period was precisely when Internet technology stocks were making new 52-week highs and trading at what appeared to be absurd valuations.

Most of the best growth stocks seldom trade at a low P/E ratio. In fact, many of the biggest winning stocks in history traded at more than 30 or 40 times earnings *before* they experienced their largest advance. It only makes sense that faster-growing companies sell at higher multiples than slower-growing companies. If you avoid stocks just because the P/E or share price seems too high, you will miss out on many of the biggest market movers. The really exciting, fast-growing companies with big potential are *not* going to be found in the bargain bin. You don’t find top-notch merchandise at the dollar store. As a matter of fact, the really great companies are almost always going to appear expensive, and that’s precisely why most investors miss out.

High Growth Baffles the Analysts

You might recall when Mark [Minervini] was here last in mid-October [1998] he recommended Yahoo!, which is up 100 percent since then. . . .

— Ron Insana, CNBC interview, November 1998

Wall Street has little idea what P/E ratio to put on companies growing at huge rates. It’s extremely difficult, if not impossible, to predict how long a growth phase will last and what level of deceleration will occur over a particular time frame when one is dealing with a dynamic new leader or new industry. Many superperformance stocks tend to move to extreme valuations and leave analysts in awe as their prices continue to climb into the stratosphere in spite of what appears to be a ridiculous valuation. Missing out on these great companies is due to misunderstanding the way Wall Street works and therefore concentrating on the wrong price drivers.

In June 1997, I bought shares of Yahoo! when the stock was trading at *938* times earnings. Talk about a high P/E! Every institutional investor I mentioned the stock to said, “No way—Ya-WHO?” The company was virtually unknown at the time, but Yahoo! was leading a new technological revolution: the Internet. The potential for what was then a new industry was widely misunderstood at the time. Yahoo! shares advanced an amazing 7,800 percent in just 29 months, and the P/E expanded to more than 1,700 times earnings. Even if you got only a piece of that advance, you could have made a boatload.

CHAPTER 7

FUNDAMENTALS TO FOCUS ON

WHEN A STOCK SUFFERS A MAJOR BREAK in price, there’s a reason, and very often it’s the beginning of lower prices to come. In almost every case, something is fundamentally wrong with the company’s business or industry. Entering 2008, many of the big banks, including Citigroup, along with their broker-dealer and investing banking cousins such as Lehman Brothers and Bear Stearns, were overleveraged and held deteriorating balance sheets. This toxic cocktail would set up the financial sector for collapse as the overall economy was stunned into a severe recession. From 2007 to 2009, former Dow component American International Group (AIG) crashed from a high of $103 down to a minuscule $0.33. On September 22, 2008, AIG was removed from the Dow Jones Industrial Index. Citigroup was removed from the Dow on June 8, 2009.

You’ve heard the old adage about buying low and selling high, so maybe you figure this is a once-in-a-lifetime opportunity—that is, to buy GE, Citigroup, or some other familiar company while it’s down in price. I bet those who bought the blue chip carmaker General Motors in 2008 felt they were getting a bargain, too. However, in just one year GM stock dropped to a level not seen since 1933, shedding almost 95 percent of its value. On June 8, 2009, General Motors was also removed from the Dow Jones Industrials Index. The fact is, no matter how big or prestigious a company is, when fundamentals deteriorate—namely, earnings—you never know how far the stock will fall.

What Drives Superperformance?

The stock market cares little about the past, including the status of a company. What it cares about is the future, namely, growth. Keep in mind that our goal is to uncover superperformance stocks: shares that will far outpace the rest of the pack. These stocks are the ones with the strongest potential, and they seldom are found in the bargain bin. They are going strong because of a powerful force behind them: growth—real growth—in earnings and sales. Why buy damaged merchandise?

If your goal is to achieve superperformance in stocks, each company must earn its place in your portfolio by being an outstanding business. Superperformance stocks show their strength through their ability to improve and grow earnings, sales, and margins. These powerhouse companies report quarterly results that are better than Wall Street anticipates, with upside surprises that propel the stock higher. Don’t become enamored with a stock selling down in price because it has a well-known name. Many

winning stocks may be companies that you never heard of before. Their best days lie ahead, not in the past. Regardless of a company’s size, status, or reputation, there is no intelligent reason for an investor to settle for an inferior track record in a marketplace filled with companies with outstanding fundamentals.

Each quarter, earnings and sales reports provide a refreshed set of statistics with new names, as those with poorer prospects are often replaced with those with greater potential. The same release of quarterly results also brings fresh data with which to evaluate the companies already in one’s portfolio. In this way, the portfolio naturally evolves to achieve its performance goal through forced displacement. Stocks that continue to deliver the goods can remain in the portfolio, and the ones that fail to perform must go.

Why Earnings?

In real estate, the mantra goes “location, location, location.” In the stock market, it’s earnings, earnings, earnings; after all, it’s the bottom line that counts. How much money can a company earn and for how long? This leads to three basic questions every investor should ask when it comes to earnings: How much? How long? and How certain? Profitability, sustainability, and visibility represent the most influential factors that move stock prices.

To understand the impact of earnings on stock prices, let’s go behind the scenes and examine how Wall Street operates. Who moves stock prices? Big institutional investors such as mutual funds, hedge funds, pension funds, and insurance companies. Many institutional investors, encompassing a relatively large number of investment professionals, use investment models that identify earnings surprises, that is, reported earnings that beat analysts’ expectations. As soon as an earnings surprise is reported, these opportunists will jump onboard or at least put the stock on their radar screens as a potential buy candidate.

Most of the big institutional investors utilize valuation models that are based on earnings estimates to determine a stock’s current worth or value. When a company reports quarterly results that are meaningfully better than expected, analysts who follow the stock must reexamine and revise

their earnings estimates upward. This increases the attention paid to a stock. The upward estimate revision is going to raise institutional investors’ projected value of the company. When earnings estimates for a stock head up, shares, of course, become more attractive—and invite buying.

Anticipation and Surprise

Stocks move for two basic reasons: anticipation and surprise. Every price movement is rooted in one of these two elements: anticipation of news, an event, an important business change, or reaction to an unexpected event and a surprise, whether positive or negative.

Anticipation means expectation, for example, rumors that a large contract may be awarded to a contractor. In anticipation of an announcement, the stock price may advance. Once the deal is on the table and the contract is officially awarded, the stock could sell off. The same thing can happen with earnings that are in line with expectations; once the announcement is made, the stock declines because that event had already been priced into or discounted in the stock price. Stocks often move in anticipation of good and bad news and then after the fact may move in the opposite direction (i.e., rallying in anticipation of a favorable development and selling off when the announcement is made). This market phenomenon may baffle newbie investors. The reason for it is that the stock market prices in future events. That is what is meant when people say the stock market is a discounting mechanism. Although anticipation moves prices, once the expected event occurs, the market sells on the news. Hence the old adage “Buy the rumor; sell the fact.”

Surprises can take many forms, from earnings that were far above or below estimates to a sudden development that significantly changes a company’s business outlook. What surprises have in common, by definition, is that they are unexpected. Suddenly, the idea of deregulating an industry catches on in Congress or a drug that seemed unlikely to win U.S. Food and Drug Administration (FDA) approval unexpectedly gets the green light. With earnings, results come in well above expectations for a positive surprise or well below for a negative surprise.

CHAPTER 9

FOLLOW THE LEADERS

MOST OF THE BIG MONEY made in bull markets comes in the early stages, during the first 12 to 18 months. However, by the time a big advance asserts itself in the broad market indexes, many of the best stocks may have been running up for weeks in advance. The question then becomes how you know when to jump on board *before* an emerging rally gets away from you and the very best stocks leave you in the dust. The answer: follow the leaders.

Top-performing stocks will lead the broader market averages at important turning points. As a bear market is bottoming, leading stocks, the ones that best resisted the decline, will turn up first and then sprint ahead—days, weeks, or even months before the Dow, S&P, and Nasdaq indexes put on their running shoes. These leading names will break into new high ground while the major indexes are just starting to come off their respective lows. At this point, overall market conditions still look bleak to most investors and the news is still for the most part negative and cautionary. Later, the rally broadens, pushing up the indexes, which propels the front-runners even higher. Then sentiment begins to shift from fear to optimism. By paying close attention to the market’s leading names, you can be in the best stocks before they are obvious to the public. This is nothing new to astute stock investors who know what to look for. The legendary Jesse Livermore built his fortune by trading in leading stocks in the 1920s and 1930s. I made 99 percent of my profits in the stock market by trading in leading names.

Market leaders tend to foretell turns to the downside as well. As a bull market enters its later stages (generally after one or two years), many of the

leadership stocks that led the market advance will start to buckle while the broad market averages march on toward their tops. Typically, a second wave of postleadership stocks start to perform relatively well as money rotates out of the true leaders and into some of the group’s constituents, laggard follow-up stocks, or defensive groups such as drugs, tobacco, utilities, and food stocks that are thought to be less sensitive to an economic downturn. Follow-on stocks and laggards, however, rarely experience the length or, more important, the magnitude of the price move that true market leaders accomplish. When you see this rotation occurring, it’s a warning that the market rally may be entering its later stage. The ultimate market top may still be weeks or even months away, but this internal market action is a proverbial shot across the bow that should get your attention.

Getting in Sync

The problem for most investors is that they fail to notice the important nuances and clues from leading stocks near turning points, and that causes them to lose perspective. Why? Investors are gun-shy after the market has been declining steadily. Just about the time the market is bottoming, most investors have already suffered large losses in their portfolios because they refused to cut their losses short. After a market correction, many investors are busy hoping to break even on the open losses they hold or are convinced that the end of the world is coming because they got crushed during the previous decline and refuse to acknowledge the buy signals individual leading stocks are offering.

Making it even more difficult is the fact that leading stocks always appear to be too high or too expensive to most investors. Market leaders are the stocks that emerge first and hit the 52-week-high list just as the market is starting to turn up. Few investors buy stocks near new highs, and fewer buy them at the correct time. They focus on the market instead of the individual market leaders and often end up buying late and owning laggards. Adding to the distraction is the fact that the news media are usually wrong at major turning points. At a market bottom they’ll predict the end of the world, and at a top the same people will say you can’t go wrong investing in stocks. It can be very confusing if you listen to what people are saying instead of pay-

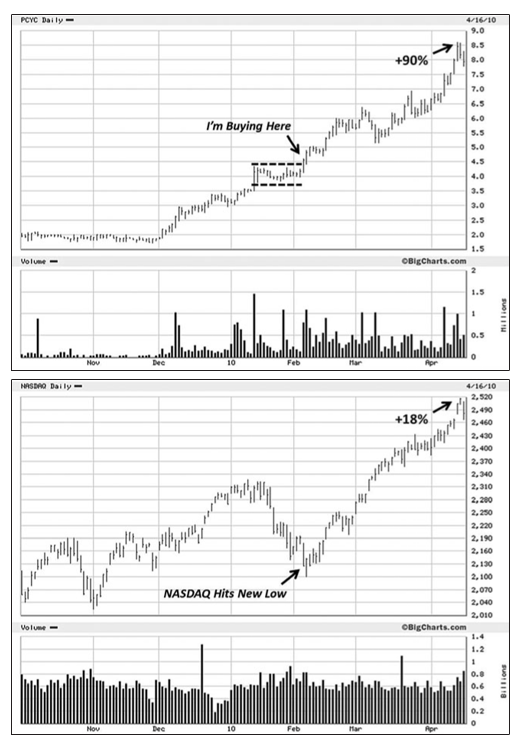

Market leader Pharmacyclics emerges into new high ground the same day the Nasdaq Composite hit a correction low. It then rose 1,500 percent in 33 months.

ing attention to what the stocks are telling you. More than 90 percent of superperformance stocks emerge from bear markets and general market corrections. The key is to do your homework while the market is down; then you will be prepared to make big profits when it turns up.

On February 4, 2010, I purchased Pharmacyclics Inc. (PCYC), and also recommended it to our Minervini Private Access clients; this was a day when the Nasdaq Composite Index was hitting a new low. Over the next 48 trading days, PCYC advanced 90 percent, during which time the Nasdaq rallied only about 18 percent. The 90 percent advance proved to be only the beginning; PCYC advanced 1,500 percent in 33 months, a clear example of market leadership.

The Lockout

During the first few months of a new bull market you should see multiple waves of stocks emerging into new high ground; general market pullbacks will be minimal and probably will be contained to 3 to 5 percent from peak to trough. Many inexperienced investors will be looking to buy a pullback that rarely materializes during the initial leg of a new powerful bull market, which from the onset will appear to be overbought.

Typically, the early phase of a move off an important bottom has the characteristics of a lockout rally. During this lockout period, investors wait for an opportunity to enter the market on a pullback, but that pullback never comes. Instead, demand is so strong that the market moves steadily higher, ignoring overbought readings. As a result, investors are essentially locked out of the market. If the major market indexes ignore an extremely overbought condition after a bear market decline and your list of leaders expands, this should be viewed as a sign of strength. To determine if the rally is real, up days should be accompanied by increased volume whereas down days or pullbacks have lower overall market volume. More important, the price action of leading stocks should be studied to determine if there are stocks emerging from sound, buyable bases.

Additional confirmation is given when the list of stocks making new 52-week highs outpaces the new 52-week low list and starts to expand significantly. At this point, you should raise your exposure in accordance with

your trading criteria on a stock-by-stock basis. As the adage goes, “It’s a market of stocks, not a stock market.” In the early stages of a market-bottom rally it’s absolutely critical to focus on leading stocks if your goal is to latch on to big winners. Sometimes you will be early. Stick with a stop-loss discipline, and if the rally is for real, the majority of the leading stocks will hold up well and you will have to make only a few adjustments. However, if you get stopped out repeatedly, you may be too early.

The Best Stocks Make Their Lows First

To make big money in the stock market, you’re going to need to have the overall stock market’s primary trend on your side. A strong market trend is not something you want to go against. However, if you concentrate on the general market solely for timing your individual stock purchases, you’re likely to miss many of the really great selections as they emerge at or close to a market bottom.

The true market leaders will show strong *relative price strength* before they advance. Such stocks have low correlation with the general market averages and very often act as lone wolves during their biggest advancing stage. The search for these stocks runs contrary to the thinking of most investors, who often take a top-down approach, examining first the economy and the stock market, then market sectors, and finally companies in a specific industry group. As I’ll show you in several examples in this chapter, many of the very best leading stocks tend to bottom and top ahead of their respective sectors, whereas specific industry groups can lead a general market turn. Although it’s true that many of the market’s biggest winners are part of industry group moves, in my experience, often by the time it’s obvious that the underlying sector is hot, the real industry leaders—the very best of the breed—have already moved up dramatically in price.

In the early stage of a relative strength leader’s uptrend, there may or may not be much confirming price strength from its group overall. This is normal. Often there will be only one or two other stocks in the group displaying strong relative strength. Therefore, it requires additional skill to pin-

point these stocks early on. As the leader’s trend continues to advance and eventually its industry group and sector begin to show signs of strength, the price advance of the market leader will do one of two things: it will continue its advance while the group propels it even higher, or it will consolidate in a sideways fashion and digest its previous gains while the group and other stocks in the group play catch-up. This does not necessarily mean that the leader’s price advance has ended, because leaders can zig while the market zags; this is typical of high alpha stocks. You should look for definite signs that the stock has topped before concluding that the move is over.

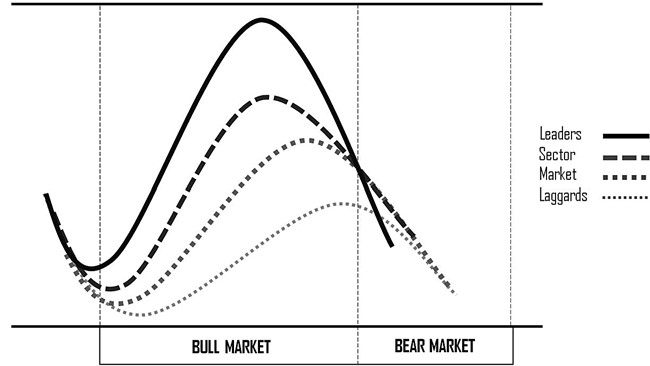

Theoretical cycle dynamics shows the leaders, the overall sector, and the laggards during a bull market and then entering a bear market phase.

CHAPTER 13

RISK MANAGEMENT

PART 2: HOW TO DEAL WITH AND CONTROL RISK

I have two basic rules about winning in trading as well as in life: (1) If you don’t bet, you can’t win. (2) If you lose all your chips, you can’t bet.

— Larry Hite

FOR THREE DECADES, enjoying eight bull markets and enduring eight bear markets, I have traded stocks; I have accumulated my personal wealth almost exclusively through stock speculation. After learning the hard lessons of experience, I have been fortunate to relish consistent success, preserving not only my original starting capital but the bulk of the gains. How will you do the same thing? In other words, how will you endure the test of time, not only winning during bull markets but preserving your gains in bear markets? The secret is neither hidden nor really a secret. The key is risk management.

Risk is the possibility of loss. When you own a stock, there is always the possibility of a price decline; as long as you are invested in the stock market, you are at risk. The goal with stock trading is to make money consistently by taking trades that have more reward potential than risk. The problem for most investors, however, is that they focus too much on the reward side and

not enough on the risk side. Simple as this sounds, few will follow the advice I’m about to impart to you.

In the stock market, everyone’s goal is to make money. To win in an environment where everyone has the same objective, you must do the things that most investors are consciously unwilling or subconsciously unable to do. If you succeed, when you look back on your career, you will see that an instrumental difference between you and them was discipline. Over time I have learned that investors don’t lose money or fail to achieve superperformance because of bear markets or economic hazards but because of mental hazards, the types of personal failings that cause you to say to yourself in retrospect, why didn’t I sell that stock when I was only down 10 percent? As you’re sitting there down 30 or 40 percent, suddenly a 10 percent loss doesn’t look so bad.

Does the following sound familiar? You bought a stock at $35 a share and were reluctant to sell it at $32; the stock then sank to $26, and you would have been delighted to sell it at the original price of $35. When the stock then sank to $16, you asked yourself, Why didn’t I sell it at $26 or even $32 when I had the chance to get out with a small loss? The reason investors get into this situation is that they lack a sound plan for dealing with risk and allow their egos to get involved. A sound plan takes implementation, which takes discipline. That part I cannot do for you, but what I can do is teach you how to do it.

Develop Lifestyle Habits

The difference between mediocrity and greatness lies in the fundamental belief that discipline is not merely a principle of trading but a principle of greatness. Managing risk requires discipline. Sticking to your strategy requires discipline. Even if you have a sensible plan, if you lack discipline, emotions will creep into your trading and wreak havoc. Discipline leads to habit. They can be good habits or bad ones; it’s a matter of what you discipline yourself to do over time. Like most people, when you get up each morning, you brush your teeth, right? You don’t say to yourself, I’m tired of

brushing my teeth over and over, so this month I’m taking a vacation from dental hygiene. To the contrary, brushing your teeth has become automatic and ingrained from years of repetition and the belief that it’s worth taking the time to do. This same type of psychological conditioning applies to such things as exercising and eating healthy, which are lifestyle habits that some people choose to make priorities in their daily lives.

If you manage your portfolio with your emotions and without discipline, prepare for a volatile, exhausting ride, probably without anything worthwhile to show for your efforts in the end. Good trading is boring; bad trading is exciting and makes the hair on the back of your neck stand up. You can be a bored rich trader or a thrill-seeking gambler. It’s entirely your choice. With intelligent repetitive work, you can cultivate successful trading habits. Making a habit of doing the things that produce positive results is worthwhile, but it requires the principle of greatness: discipline.

Contingency Planning

Success is never final.

— Winston Churchill

In the stock market and in life, risk is unavoidable. The best anyone can do is to manage risk through sensible planning. The only way to control risk when investing in stocks is through how much we buy and sell, when we buy and sell, and how we prepare for as many potential events as possible. As a stock market investor, you must learn to sell for your own protection because you have no control over the forces that move stock prices. Your goal is not risk avoidance but risk management: to mitigate risk and have a significant degree of control over the possibility and amount of loss.

I don’t like to leave anything to chance in my trading. If I go into a casino and play blackjack, I know what the odds are, and if I feel like taking a chance, that’s the best I can hope for. But I don’t gamble with stock trading, which would be rolling the dice with my livelihood and my security. The best way to ensure stock market success is to have contingency plans

and continuously update them as you learn and encounter new scenarios. Your goal should be to trade without hassles and surprises. To do that, you need to develop a dependable way to handle virtually every situation that is thrown at you. Having things thought out in advance is paramount to managing risk effectively.

The mark of a professional is proper preparation. To execute, you must be prepared. Before I invest, I have already worked out in advance responses to virtually any conceivable development that may take place. I can’t think of an event that I’m not prepared for. If and when new circumstances present themselves, I add them to my contingency plans; as new unexpected issues present themselves, the contingency plan playbook is expanded.

By implementing contingency planning in advance, you can take swift, decisive action the instant one of your positions changes its behavior or is hit with an unexpected event. You should also be prepared to deal with profits when they come to fruition. Before the open of each trading day, mentally rehearse how you will handle each position based on whatever could potentially unfold during that day. Then, when the market opens for trading, there will be no surprises; you already know how you will respond.

You should run your portfolio the way an airline pilot operates a 747 jumbo jet. To ensure the safe passage of the flight, the pilot has advance plans for every possible contingency: engine failure, severe weather conditions, hydraulic malfunction, and hundreds of other mechanical or electronic problems. The pilot has considered possibilities ranging from an electrical storm to trouble with one of the passengers. When a problem occurs, there is no debate or delay. For every eventuality, the pilot has a procedure or countermeasure. This comes from training and preparation. When we’re not prepared, we’re vulnerable. September 11, 2001, was a grim reminder of the importance of proper preparation. As a result, cockpit doors are now fortified, and the sky marshal program put into place during the 1960s has been expanded. Some pilots are even armed. Learning from our past mistakes and being properly prepared allow for safer travel and for safer investing as well.

I have the following four basic contingency plans for my stock trading.

The Initial Stop-Loss

Before buying a stock, I establish in advance a maximum stop loss: the price at which I will exit the position if it moves against me. The moment the price hits the stop loss, I sell the position without hesitation. Once I’m out of the stock, I can evaluate the situation with a clear head. The initial stop loss is most relevant in the early stages of a position. Once a stock advances, the sell point should be raised to protect your profit with the use of a trailing stop or back stop.

The Reentry

Some stocks set up constructively and may even emerge from a promising base and attract buyers but then quickly undergo a correction or sharp pullback that stops you out. This tends to occur when the market is experiencing general weakness or high volatility. However, a stock with strong fundamentals can reset after such a correction or pullback, forming a new base or a proper setup. This show of strength is a favorable sign. Often, the second setup is stronger than the first. The stock has fought its way back and along the way shaken out another batch of weak holders. If it breaks out of the second base on high volume, it can really take off.

You shouldn’t assume that a stock will reset if it moves against you. You should always protect yourself and cut your loss. However, if a stock knocks you out of your position, don’t automatically discard it as a future buy candidate. If the stock still has all the characteristics of a potential winner, look for a reentry point. Your timing may have been off. It could take two or even three tries to catch a big winner. This is a trait of professional traders. Amateurs are scared of positions that stop them out once or twice or just weary of the struggle; professionals are objective and dispassionate. They assess each trade on its merits of risk versus reward; they look at each trade setup as a new risk or a new opportunity. Some believe that selling a stock and then reentering the same stock soon afterward is amateurish. I believe missing opportunity because of emotion is as amateurish. Managing risk with the use of stop losses, particularly in a whipsaw market, can sometimes give a trader the feeling of chasing one’s tail. Recognize the feelings of frustration and then remind yourself not

to let ego override good risk management. So you got it wrong the first time—big deal. So you got it wrong the second time—clever fish! Laugh and keep your rod and reel ready. It’s the long-term results that count. Some of my best trades were in stocks that previously stopped me out several times and then reset.

Selling at a Profit

Once a stock amasses a percentage gain that is a multiple of your stop loss, you should rarely allow that position to turn into a loss. For instance, let’s say your stop loss is set at 7 percent. If you have a 20 percent gain in a stock, you shouldn’t allow that position to give up all that profit and produce a loss. To guard against that, you could move up your stop loss to breakeven or trail a stop to lock in the majority of the gain. You may feel foolish breaking even on a position that was previously a decent gain; however, you will feel even worse if you let a nice gain turn into a loss.

At some point you have to close out a trade. There are two ways you can sell:Into strength, which means cashing out shares while the share price is risingInto weakness, which means selling while the share price is declining

Selling into strength is a learned practice of professional traders. It’s important to recognize when a stock is running up rapidly and may be exhausting itself. You can unload your position easily when buyers are plentiful. Or you could sell into the first signs of weakness immediately after such a price run has broken down. You need to have a plan for both selling into strength and selling into weakness.